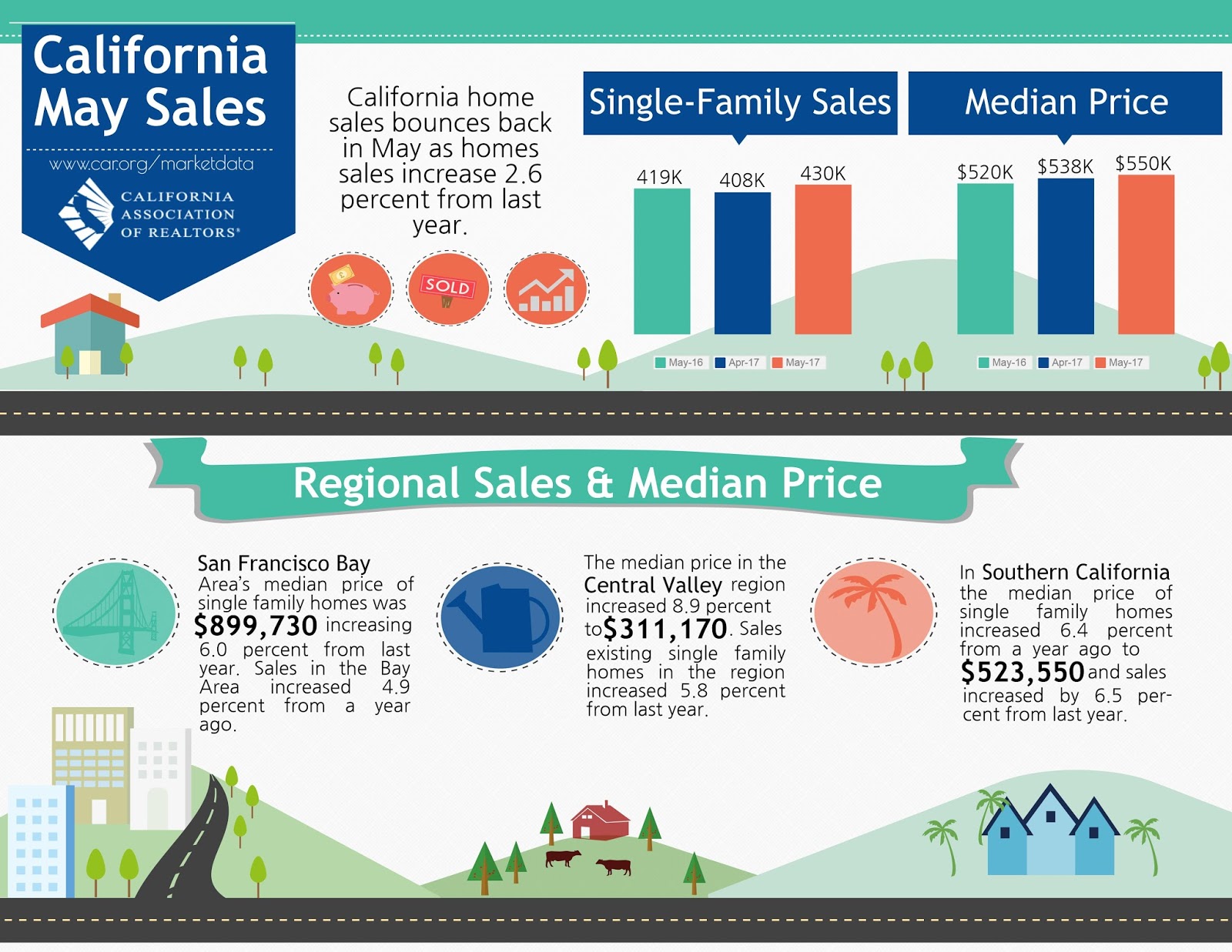

You’ve been spending so much time on projects inside your home (like that new shower you have to drag yourself out of), that your front yard is starting to scream for a bit of attention.

Poor neglected, thing.

You know your yard has some super curb appeal potential, but where to begin?

Check out the National Association of REALTORS®’ 2016 Remodeling Impact Report: Outdoor Features (full disclosure: NAR is HouseLogic’s sponsor). It’s got some interesting data on how landscaping affects home value, especially those with tons of curb appeal. They beat out all indoor projects when it comes to adding value to your home!

Below are four projects with so much curb-appeal juice, any money you invest in them is likely to pay you back much more.

#1 Add or Replace a Few Design Basics

Every few years, you overhaul your closet, replacing your worn-out basics with a few new pieces to ramp up your wardrobe. Why not do the same with your yard? Give it a basic makeover so it has some good, classic, value-boosting “bones” to build upon.

Landscape design basics like:

• A winding flagstone walkway

• A couple of stone planters (6 feet by 2 feet)

• A few flowering shrubs

• A deciduous tree about 15 feet tall

• Quality mulch

Why you can’t go wrong: The median cost for this makeover is $4,750. But the recoup (how much more your house would sell for after doing this project) is $5,000! Pretty sweet, right?

#2 Add Color and Texture in the Right Places

Experts call it “softscaping.” But basically, it’s adding plants in a designed, intentional way that makes your yard interesting to look at year-round.

It’s a great project if your yard is already in pretty good shape with some basic design elements mentioned above.

A typical softscaping project includes:

• Five trees

• 25 shrubs

• 60 perennials

• Natural edging

• Boulder accents

Why you can’t go wrong: You’ll invest about $7,000, but you could recoup every cent in home value, according to the Report. Plus, here’s what the report doesn’t include: You’ll get super energy savings.

Who doesn’t love lower utility bills?

Just three trees in the right location can save up to $250 a year in heating and cooling costs, says the source for energy-saving stats: the U.S. Department of Energy.

Shade trees help boost curb appeal

#3 Build a Deck or Patio if You Don’t Have One

If you’re spending sunny days admiring the great outdoors from indoors, it’s time for a change to get you outside… like finally building that deck or patio you’ve been dreaming of.

Why you can’t go wrong: A patio costs about $6,400 and recoups 102%. A wood deck will cost $9,450 with a slightly higher recoup of 106%. Plus, how can you put a price on all those evening cookouts and Sunday brunches al fresco?

#4 Heap Loads of Love on Your Lawn

Yep, you read that right. Especially if you know you’re going to sell in the next year or so.

It’s the easiest project to do — and it has a whopping ROI of 303%!

Lawn maintenance is simple:

• Fertilize

• Aerate

• Weed

• Rake

Why you can’t go wrong: It’s the cheapest project to do with an annual cost of only $330. Every year, you’ll reap the benefits of a lush, barefoot-friendly lawn.

(But note that unlike the other landscaping features listed in this article — deck, patio, hardscaping, trees, etc. — you’ll only get that fabulous 303% ROI on your maintenance costs for the year right before you sell. That’s because lawn maintenance has to be repeated annually, unlike the other projects).