Showing posts with label #beverlyhillsrealestate #brentwood. Show all posts

Showing posts with label #beverlyhillsrealestate #brentwood. Show all posts

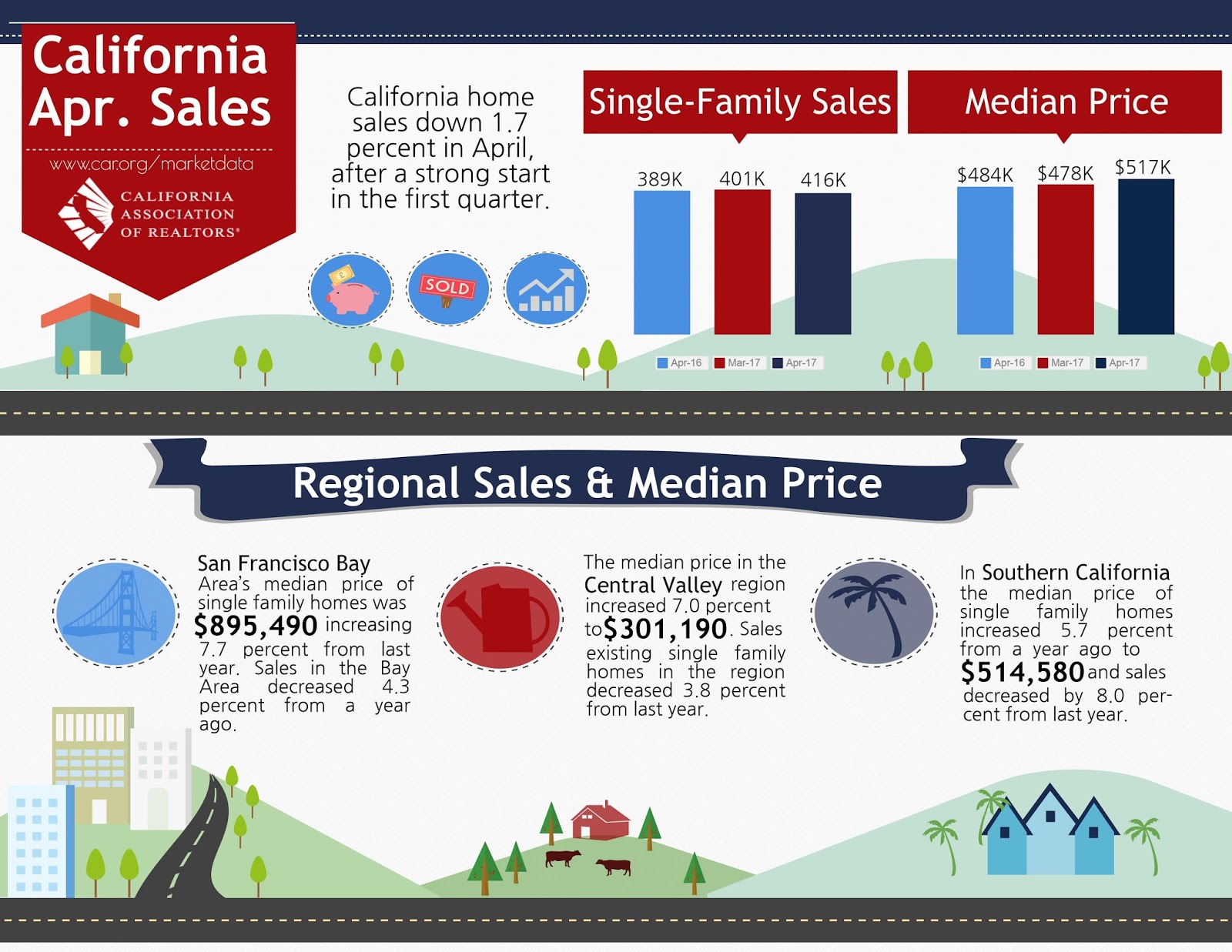

Monday, May 22, 2017

Monday, November 16, 2015

Deductions for Homeowners

What's Deductible? -- A to Z

Acquisition debt. See Mortgage interest.

Advertisement

Boats as homes. A boat that has eating, sleeping and sanitary facilities can qualify as a first or second home, so you can deduct mortgage interest paid on the loan secured by the boat to buy it. However, if you are subject to the alternative minimum tax, this write-off is not allowed.

Cancelled debt on foreclosure or short sale. Generally, when a debt is canceled or forgiven, the borrower is considered to have received taxable income equal to the amount of the canceled debt. However, through 2012, up to $2 million of debt discharged on a mortgage on a principal residence -- in a foreclosure, for example, or short sale -- can be tax-free.

Casualty loss. If your home was damaged or destroyed -- by fire or storm, for example -- you may be able to get financial help from Uncle Sam by deducting a casualty loss on your return. Your deduction for a 2010 loss is generally the total of your unreimbursed loss reduced by $500 100 and further reduced by 10% of your adjusted gross income.

Depreciation on home. Profit due to depreciation claimed on your residence before May 7, 1997 -- because you had a home office, for example, or at one time rented out the property -- qualifies for the rule that lets you treat $250,000 of home sale profit as tax-free income. (The limit is $500,000 if you're married and file a joint return.) Profit due to depreciation after May 6, 1997, is taxed at 25%, unless you're in a lower tax bracket, in which case that rate applies.

Discharged debt. See Cancelled debt on foreclosure or short sale.

D.C. first-time homebuyer credit. If you bought a home in the nation's capital during 2010, you may be eligible for a $5,000 tax credit. It doesn't really have to be your first home ... just a home you purchased in the District of Columbia after not owning one in D.C. for at least one year. It doesn't matter if you have owned a home elsewhere. This break phases out as income exceeds $70,000 on single returns and $110,000 on married filing jointly returns. See first-time homebuyer credit. If you bought during the part of 2010 when the nationwide homebuyer credit was available (see below), you must choose between the two credits. You can’t claim both.

Energy credits. You can earn a 2009 tax credit for installing energy-saving home improvements such as new doors, new windows, energy-efficient furnaces, heat pumps, hot water heaters, air conditioners, etc. The credit is 30% of the cost of installing such energy savers, up to a top credit of $1,500. For windows and doors, the credit is based on the cost of the materials; for furnaces and air conditioners and the like, you can count the cost of installation, too. A bigger credit is available for more ambitious projects – like solar hot-water heating systems, geothermal heat pumps and, yes, even residential wind energy systems. Start generating your own power and Uncle Sam will rebate 30% of the full cost of your system…with no dollar cap.

First-time homebuyer credit. If you bought a home during the first four months of 2010, you may qualify for either an $8,000 or $6,500 home buyer credit. And, you don’t really have to be a first-time home buyer to qualify for either credit. To qualify for the $8,000 credit you (and your spouse if married) must not have owned a home in the three years leading up to the purchase of your new home. The credit is 10% of the purchase price of the home, up to a maximum credit of $8,000. No credit is allowed for homes that cost more than $800,000.

To qualify for the $6,500 credit, you must be a long-time homeowner, defined as owing and living in the same principal residence for five of the eight years leading up to the purchase of your new home. The credit is 10% of the purchase price of the home, up to a maximum credit of $6,500. No credit is allowed for homes that cost more than $800,000.

Timing is everything. To qualify for either credit, you must have signed a binding contract on your new home before May 1, 2010, and you must have closed on the deal by September 30, 2010.

Unlike a first-time home buyer credit available in 2008 – which had to be paid back over 15 years by adding $500 in each of those years to the taxpayer’s tax bill – the 2010 credit does not have to be paid back, as long as you live in the principal residence for at least three years.

First-time homebuyer credit repayment. The $7,500 first-time homebuyer credit that was available for qualifying purchases after April 8, 2008, and before January 1, 2009, must be repaid starting with your 2010 tax return. To repay this “interest-free loan”, you must add $500 each year to your tax bill until the full $7,500 is repaid. If you sell or otherwise stop using the house as your home before the credit is fully repaid, any remaining balance must be repaid with your tax return for the year of the sale.

Foreclosure. See Cancelled debt on foreclosure or short sale.

Home-equity debt. Interest on up to $100,000 of debt secured by your first or second home -- using a second mortgage, say, or home equity line of credit -- can be deducted, regardless of how the money is used. The use of home-equity debt gives homeowners an opportunity to skirt the rules that generally block the deduction of debt used to buy automobiles, for example, or pay for vacations.

Home-office deduction. You can deduct the costs of a home office that you use exclusively and regularly for business. This includes depreciation, utilities and insurance for the office portion of your home. To qualify for the tax break you must either meet with clients there regularly, or the home office must be your principal place of business (unless it is not attached to your house).

Home-sale exclusion. Up to $250,000 of profit from the sale of your home can be tax free; $500,000 if you are married an file a joint return. To qualify, you must own and live in the house for periods totaling two years out of the five years leading up to the sale. A reduced exclusion is available if you fail the two-year test due to unforeseen circumstances such as a move resulting from a job change, for example, or divorce. You can use this exclusion any number of times but no more frequently than once every two years.

IRA payouts for first-time homebuyers. You can withdraw as much as $10,000 from a traditional IRA before age 59½ without penalty if the money is used to buy the first home for yourself, a child or grandchild, or your parents or grandparents. Although the payout avoids the normal 10% early-withdrawal penalty, it is taxed. Different rules apply to tapping a Roth IRA for the purchase of a home. See Roth IRA payouts for first-time homebuyers.

Loan prepayment penalties. If your lender charges you a penalty for prepaying your mortgage early, the charge is deductible as mortgage interest.

Mortgage interest. You can deduct interest on up to $1.1 million of loans used to buy or build or improve your first or second home and secured by the property. Up to $1 million of such debt is called acquisition debt, which must be used to acquire or improve the property, and up to $100,000 more is called home equity debt, which can be used for any purpose.

Mortgage interest credit. If you received a mortgage credit certificate from a state or local governmental agency, you can claim a tax credit of up to $2,000 of mortgage interest paid.

Moving expenses. If a move is connected with taking a new job that is at least 50 miles farther from your old home than your old job was, you can deduct travel and lodging expenses for you and your family and the cost of moving your household goods. If you drive your own car, you can deduct 24 16.5 cents a mile for 2009 2010 moves. (For 20102011, the standard mileage rate for moving is 16.519 cents a mile.) If you moved to take your first job, the 50-mile test applies to the distance between your old home and your new job. The deduction is allowed even if you do not itemize deductions.

Parsonage allowance. For members of the clergy, the value of a home provided by the church is a tax-free fringe benefit. A housing allowance is also tax-free.

Points. Points you pay to get a mortgage for your principal residence are generally fully deductible in the year paid, even if you persuade the seller to pay your points for you. They are not deductible if paid as part of a refinancing a mortgage on your principal home or on a second home; in that those cases, you deduct the points over the life of the loan.

Presidentially declared disaster. If your home was damaged or destroyed in an area that the President declared a disaster area, special rules apply to the casualty loss deduction. For one thing, for 2009 losses the law waives the requirement that you reduce your loss by an amount equal to 10% of your adjusted gross income to arrive at the deduction. And, youYou may choose to deduct your loss in the year it occurred or the previous year, whichever is more advantageous. If you claim a 2010 loss on a 2009 amended return, for example, you’ll get your tax savings via a refund check from the IRS.

Property taxes. See Real estate taxes.

Real estate taxes. You can deduct state and local real estate taxes paid during the year on any number of personal residences you own. (A 2009 break that allowed homeowners who claimed If you choose to claim the standard deduction rather than itemize deductions, you canto boost their standard deduction to include some of the property tax they paid was not renewed for 2010.)add $500 if single or $1,000 if married filing jointly to the regular standard deduction amount if you paid at least that much in state and local real estate taxes. If you own rental properties, real estate taxes on them are deducted on Schedule E where you report rental income.

Real estate taxes when you buy a home. If you bought a home during the year, check to see if the seller had prepaid property taxes for a period you actually owned the home. If so, include that amount in your property tax deduction for the year . . .even if you did not reimburse the seller.

Recreational vehicle. If your RV has cooking, sleeping and sanitation facilities, interest on a loan used to buy it can qualify as deductible mortgage interest on a first or second home. If you are subject to the alternative minimum tax, interest on an RV loan is not deductible.

Refinancing points. Generally, points paid when refinancing are deducted over the term of the loan. But if you refinanced a loan that you previously refinanced, you can deduct in full the as-yet-undeducted points remaining on the prior loan. There's a catch, however: If you refinanced with the same lender, the remaining points must be amortized over the term of the new loan.

Rehabilitation credit. If your residence is certified by the government as a historic building, you can claim a tax credit for 20% of the cost of renovating it. The renovation must be substantial, and the expenses must be incurred within a 24-month period.

Reverse mortgage. Amounts received under a reverse mortgage -- either a lump sum payment or periodic payments -- are tax free. Interest that accrues on a reverse mortgage is not deductible until it is paid, and then only interest on up to $100,000 of debt can qualify.

Roth IRA payouts for first-time homebuyers. Because the rules for the Roth IRA allow you to withdraw contributions at any time without penalty, the Roth can be a powerful tool for saving for a first home. Say you and your spouse each put $5,000 a year into a Roth for five years. The entire $50,000 could be withdrawn tax- and penalty-free for a down payment and, because the accounts have been opened for at least five years, up to $10,000 of earnings can be withdrawn tax- and penalty-free if used to buy your first home.

Serial refinancers.If you refinanced in 2010 and paid off a home mortgage you acquired when refinancing to pay off an earlier mortgage, any as-yet-undeducted points on the previous refinancing may be deductible on your 2010 return. See Refinancing points.

Tax-free profit. See Home sale exclusion.

Tax-free profit on vacation home. Because you can use the home-sale exclusion repeatedly, it's possible to make profit on a vacation home tax free. If you move into the place and live there for two of the five years prior to selling it, you can qualify to claim up to $250,000 of profit tax free (up to $500,000 if you are married and file a joint return).

A recent change in the law, however, has diluted the potential value of this break. For vacation homes converted to principal residences after December 31, 2008, a portion of the gain will be taxed. The taxable part will be based on the ratio of the time after 2008 when the house was a second home or a rental to the total time you owned it.

Tax-free rental income. If you rent out your home for 14 or fewer days during the year -- when there's a major sporting event or political convention in your hometown, for example -- the rental income is tax-free, regardless of how much you make.

Vacation home. Mortgage interest on your second home is deductible, just as it is for your principal residence. Property taxes can be deducted on any number of homes. If you rent the place for 14 or fewer days during the year, the rental income is tax-free to you. If you rent it for more than 14 days a year, you must report the income, but also may claim deductions for rental expenses.

Thursday, June 4, 2015

5 reasons you still need a real-estate agent

You might think buying or selling on your own will save money, but it could be more costly in the long run.

The proliferation of services that help home buyers and sellers complete their own real-estate transactions is relatively recent, and it may have you wondering whether using a real-estate agent is becoming a relic of a bygone era. While doing the work yourself can save you the significant commissions that many real-estate agents command, for many, flying solo may not be the way to go — and could end up being more costly than a commission in the long run. Buying or selling a home is a major financial and emotional undertaking. Find out why you shouldn't discard the notion of hiring an agent just yet.

1. Better access/more convenience

A real-estate agent's full-time job is to act as a liaison between buyers and sellers. This means that he or she will have easy access to all other properties listed by other agents and will know what needs to be done to get a deal together. For example, if you are looking to buy a home, a real-estate agent will track down homes that meet your criteria, get in touch with sellers' agents and make appointments for you to view the homes. If you are buying on your own, you will have to play this telephone tag yourself. This may be especially difficult if you're shopping for homes that are for sale by owner.

A real-estate agent's full-time job is to act as a liaison between buyers and sellers. This means that he or she will have easy access to all other properties listed by other agents and will know what needs to be done to get a deal together. For example, if you are looking to buy a home, a real-estate agent will track down homes that meet your criteria, get in touch with sellers' agents and make appointments for you to view the homes. If you are buying on your own, you will have to play this telephone tag yourself. This may be especially difficult if you're shopping for homes that are for sale by owner.

Similarly, if you are looking to sell your home yourself, you will have to solicit calls from interested parties, answer questions and make appointments. Keep in mind that potential buyers are likely to move on if you tend to be busy or don't respond quickly enough. Alternatively, you may find yourself making an appointment and rushing home, only to find that no one shows up.

2. Negotiating is tricky business

Many people don't like the idea of doing a real-estate deal through an agent and think that direct negotiation between buyers and sellers is more transparent and allows the parties to look after their own interests better. This is probably true — assuming that both the buyer and seller are reasonable people who are able to get along. Unfortunately, this isn't always an easy relationship.

Many people don't like the idea of doing a real-estate deal through an agent and think that direct negotiation between buyers and sellers is more transparent and allows the parties to look after their own interests better. This is probably true — assuming that both the buyer and seller are reasonable people who are able to get along. Unfortunately, this isn't always an easy relationship.

What if you, as a buyer, like a home but despise its wood-paneled walls, shag carpet and lurid orange kitchen? If you are working with an agent, you can express your contempt for the current owner's decorating skills and rant about how much it'll cost you to upgrade the home without insulting the owner. For all you know, the owner's late mother may have lovingly chosen the décor. Your real-estate agent can convey your concerns to the seller’s agent. Acting as a messenger, the agent may be in a better position to negotiate a discount without ruffling the homeowner's feathers.

|

A real-estate agent can also play the “bad guy” in a transaction, preventing the bad blood between a buyer and seller that can kill a deal. Keep in mind that sellers can reject a potential buyer's offer for any reason — including just because they hate his or her guts. An agent can help by speaking for you in tough transactions and smoothing things over to keep them from getting too personal. This can put you in a better position to get the house you want. The same is true for the seller, who can benefit from a hard-nosed real-estate agent who will represent his or her interests without turning off potential buyers who want to niggle about the price.

3. Contracts can be hard to handle

If you decide to buy or sell a home, the offer-to-purchase contract is there to protect you and ensure that you are able to back out of the deal if certain conditions aren't met. For example, if you plan to buy a home with a mortgage but you fail to make financing one of the conditions of the sale — and you aren't approved for the mortgage — you can lose your deposit on the home and could even be sued by the seller for failing to fulfill your end of the contract. (Keep in mind that the details of any contract may vary based on state law.)

An experienced real-estate agent deals with the same contracts and conditions on a regular basis and is familiar with which conditions should be used, when they can be removed safely and how to use the contract to protect you, whether you're buying or selling your home.If you decide to buy or sell a home, the offer-to-purchase contract is there to protect you and ensure that you are able to back out of the deal if certain conditions aren't met. For example, if you plan to buy a home with a mortgage but you fail to make financing one of the conditions of the sale — and you aren't approved for the mortgage — you can lose your deposit on the home and could even be sued by the seller for failing to fulfill your end of the contract. (Keep in mind that the details of any contract may vary based on state law.)

4. Real-estate agents can't lie

Well, OK, actually they can. But because they are licensed professionals, there are more repercussions if they do than for a private buyer or seller. If you are working with a licensed real-estate agent under an agency agreement, such as a conventional, full-service commission agreement in which the agent agrees to represent you, your agent will be bound by law to a fiduciary relationship. In other words, the agent is bound by law to act in his clients' best interest, not his own.

In addition, most real-estate agents rely on referrals and repeat business to build the kind of client base they'll need to survive in the business. This means that doing what's best for their clients should be as important to them as any individual sale.

Finally, if you do find that your agent has gotten away with lying to you, you will have more avenues for recourse, such as through your agent's broker or professional association or possibly even in court if you can prove that your agent has failed to uphold his fiduciary duties.

When a buyer and seller work together directly, they can — and should — seek legal counsel, but because each is expected to act in his or her best interest, there isn't much you can do if you find out later that you've been duped about multiple offers or the home's condition. And having a lawyer on retainer any time you want to talk about potentially buying or selling a house could cost far more than an agent's commissions by the time the transaction is complete.

5. Not everyone can save money

Many people eschew using a real-estate agent in order to save money, but keep in mind that it is unlikely that both the buyer and seller will reap the benefits of not having to pay commissions. For example, if you are selling your home on your own, you will price it based on the sale prices of other comparable properties in your area. Many of these properties will be sold with the help of an agent. This means that the seller gets to keep the percentage of the home's sale price that might otherwise be paid to the real-estate agent.

However, buyers who are looking to purchase a home sold by owners may also believe they can save some money on the home by not having an agent involved. They might even expect it and make an offer accordingly. However, unless buyer and seller agree to split the savings, they can't both save the commission.

The bottom line

While there are certainly people who are qualified to sell their own homes, taking a quick look at the long list of frequently asked questions on most “for sale by owner” websites suggests the process isn't as simple as many people assume. And when you get into a difficult situation, it can really pay to have a professional on your side

Thursday, December 4, 2014

Staging Your Home For A Successful Sale

Staging plays up your home's good features, such as enhancing a great view or drawing the buyer's eye to some spectacular wood floors. It also helps to minimize some of the home's drawbacks, such as making a small bedroom look larger. But also understand that staging does not in any way mean concealing structural defects, such as hanging a picture over a water stain or putting curtains over a broken window!

Staging allows a potential buyer to visualize what can be done with the home, which is especially important with a house that's currently vacant. For example, some carefully arranged furniture in a room that would otherwise be empty can really help the buyer see the room's potential. And if you're in a neighborhood of tract houses that all look pretty much the same inside, good staging will set your home apart from the others for sale in the neighborhood.

Finally, good staging makes buyers feel at home. It lets them really imagine themselves in the kitchen with friends, or relaxing in front of the living room fire, or even working on their car in the garage.

Remove Clutter

There are several things that go into staging a home for sale, and probably the single most important one is getting rid of all the clutter. No one wants to see several days' worth of mail and newspapers on the kitchen counter, or a kid's bedroom crammed with toys and games. The same applies to the garage, basement and even the backyard storage shed.

Clutter is not just an overflowing magazine rack. It can be too many pictures on the wall, too many chairs wedged around the dining room table, or an oversized sofa that blocks the living room traffic patterns. It can be too many items of clothing crammed into a closet, or too many of grandma's dishes filling up every inch of a kitchen cabinet.

When decluttering the house, stuffing everything into the closet or in boxes in the garage is not the answer. Remember that a potential buyer is looking in every nook and cranny of the house, and an overflowing closet doesn't make much of an impression. Instead, get the clutter completely out of the house. This could be a garage sale, some donations to a local charity, or simply a trip to the landfill. If you still have items that are cluttering up the house but they are things you'll want for your next home, then rent a temporary storage space and move them there.

Let Buyers Envision Themselves There

In addition to removing the clutter to make the rooms feel more open and the closets and cabinets feel more spacious, you want to always have an eye on what things you can do to help the buyers visualize living there. For example, lots of family photos on the wall will make it hard for the buyers not to feel like they're trespassing in someone else's home.

Likewise, while you may be very proud of your religious affiliations, your choice of political ideologies, or your gun collection and the elk head on the wall, remember that not everyone shares your interests. If you can depersonalize the home to some degree, it will make it easier for potential buyers to see themselves making a life there.

Your home should also be absolutely immaculate when you have it on the market for sale. Clean the counters and the cabinets and the fixtures and the flooring and every other part of the house until it shines. Wash the windows, let in the light, and make sure that beautiful view or that inviting backyard is clearly visible when a buyer walks through. A clean house also gives potential buyers more confidence that the structure of the house has been properly maintained and cared for as well.

Hire a professional stager

It often makes good financial sense to hire a professional to do the staging for you. A professional home staging company will thoroughly understand the concepts of space and light and color, and they know how to make rooms show off to their full potential. They also don't have the same personal attachment to the home and its furnishings that you do, so they can make practical, impartial suggestions that you might otherwise overlook or simply not want to face.

The cost of professional staging varies with the size of the house and amount of work involved, but a well-staged home should sell quicker and for more money, which makes that upfront expense a wise financial investment.

Subscribe to:

Posts (Atom)